A mature and accessible technology

No high tech: applicable to all types of roofs, in new build or renovation. Return on investment: 3–7 years depending on the regions.

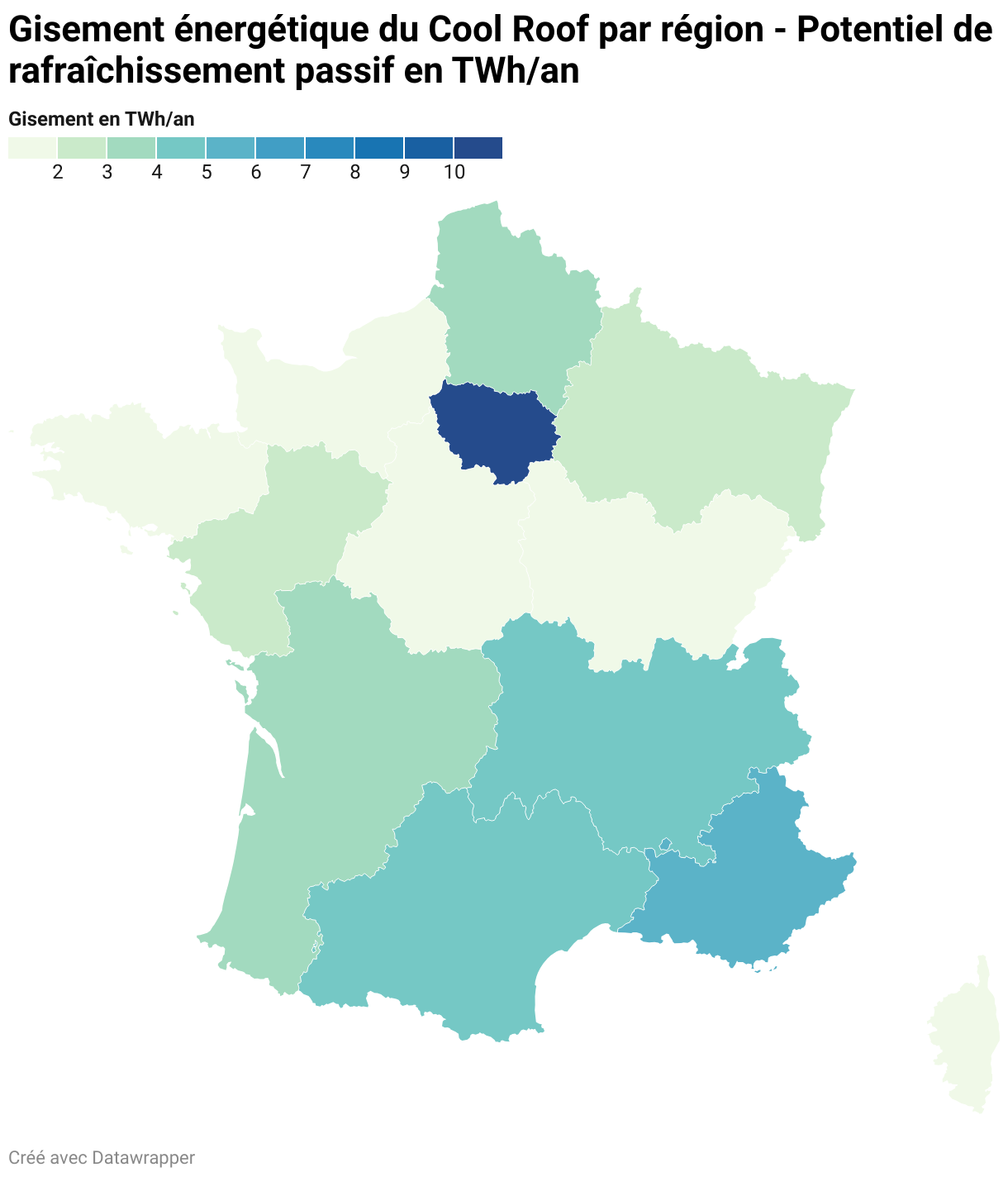

“43.9 TWh/year represents a credible alternative to large energy projects, faster and less restrictive than nuclear power.# Cool Roof: Île-de-France in the lead, Auvergne-Rhône-Alpes surprises

As France seeks solutions to reduce its summer energy consumption, a simple yet effective technology is emerging: the cool roof or “cool roof”. Our analysis reveals a national potential of 43.9 TWh per year, equivalent to 3.4 EPR reactors or ≈195% of French solar production (22.7 TWh in 2023).

Île-de-France, the unexpected champion of cooling

With 11.1 TWh/year, Île-de-France alone accounts for 25.3% of the national potential. This is explained by the exceptional concentration of its tertiary building stock : 247 million m² of offices, shops and public buildings.

“This Île-de-France dominance perfectly illustrates the urban challenge of the cool roof. Paris and its region concentrate 30% of France's GDP on just 2.2% of the territory, with 2,100 m² of tertiary space per km² – 26 times the national average.“

The South takes advantage of its climate… but Auvergne-Rhône-Alpes surprises

Behind Île-de-France, the Mediterranean regions stand out thanks to a climate factor increased by 20%. Provence-Alpes-Côte d'Azur (5.1 TWh/year) and Occitanie (4.6 TWh/year) occupy the 2nd and 3rd places respectively.

But the surprise comes from Auvergne-Rhône-Alpes, which rises to 4th place with 4.2 TWh/year, even surpassing some southern regions! A surprising result for a region with a temperate climate, but explained by its substantial tertiary building stock : 94 million m² divided among Lyon (France's 2nd economic metropolis), Grenoble (technopole), and a network of dynamic mid-sized towns.

“AURA perfectly illustrates that mass can compensate for climate", our analysis notes."With 94 million m² of tertiary surfaces, as much as PACA, the region makes up for its climatic disadvantage through sheer volume.“

This climate bonus reflects a physical reality: the hotter it is, the more effective the cool roof. By absorbing less solar radiation, these white or reflective roofs exponentially reduce air‑conditioning needs.

Overseas departments (DOM), territories with high specific potential

The overseas territories show a factor +30%. Out of 35.1 million m² of tertiary space (3.6% of the total), we obtain 2.05 TWh/year (4.7% of the potential):

- Guadeloupe : 0.50 TWh/year

- Martinique : 0.48 TWh/year

- French Guiana : 0.46 TWh/year

- Réunion : 0.44 TWh/year

- Mayotte : 0.23 TWh/year

Major economic challenge: in these territories where electricity costs €0.15–0.25/kWh (vs €0.10/kWh in mainland France), the cool roof generates doubled savings compared to mainland France.

What is a cool roof?

Turning dark roofs into light/reflective surfaces (white paints, membranes, greening) reduces solar absorption by 80%.

Result: 20–50 °C drop in surface temperature, savings of 45 kWh/m²·year. Depending on the type (flat, pitched, vegetated) and the environment (urban vs rural), these gains range from 30 to 60 kWh/m²·year.

Note: expect about a 10% albedo loss after 5 years without maintenance.

An opportunity with multiple benefits

Beyond energy savings, the cool roof generates co-benefits considerable:

- Reduction of the urban heat island : -2 to 5°C in cities

- Improved comfort : more stable indoor temperatures

- Extended lifespan of roofs (less expansion)

- Reduction of CO₂ emissions : less air conditioning = less electricity

Challenges and prospects: when Lyon competes with Marseille

This mapping also reveals the territorial disparities surprising ones. While Île-de-France could save the equivalent of 11 TWh, Brittany tops out at 1.7 TWh. But the case of Auvergne-Rhône-Alpes challenges preconceived notions: without benefiting from the Mediterranean “climate bonus,” the region secures a potential of 4.2 TWh thanks to its exceptional economic development.

Lyon, 2nd French tertiary hub, concentrates headquarters, data centers and business districts. Grenoble brings its technological ecosystem, while cities like Annecy, Chambéry or Saint-Étienne swell the regional building stock. Result: AURA literally 'dries up' its southern competitors in terms of volume!

The dense urban areas (Lyon, Marseille, Toulouse) emerge as priority targets, combining floor area volume and climate efficiency. Conversely, rural areas, despite more limited potential, could benefit from investment costs being more accessible.

A competitive cool roof economy

Investment cost: €15–25/m² depending on the technique (reflective paint vs high-performance membrane).

For the 976 million m² in France: total investment of €14.6 to €24.4 billion.

Comparison with other energy sources:

| Solution | Total investment | Annual production | Cost per TWh |

|---|---|---|---|

| Cool roof technology | €14.6-24.4 billion | 43.9 TWh/year | €330-560M/TWh |

| Solar park 1 TWh/year | €800M-€1.2B | 1 TWh/year | €800M-€1.2B/TWh |

| Wind farm 1 TWh/year | €650M-€900M | 1 TWh/year | €650-900M/TWh |

| EPR (Flamanville 3) | €19B | 13 TWh/year | €1.46B/TWh |

Spectacular result: the cool roof shows a cost 2 to 4 times lower per TWh! At €330–560M/TWh, it is the most competitive energy solution on the French market.

Methodology and limitations

Based on 976 million m² of tertiary buildings (ADEME 2023) and 45 kWh/m²·year (ADEME/DOE/EPA references). Climatic factors (1.0; 1.2; 1.3) to be refined by basin. Albedo effectiveness over time and roof typology must be integrated to move from a linear estimate to an operational analysis.

Sources: ADEME, CEREMA, INSEE – Produced: analysis based on 2023–2024 energy statistics

Art of Roof internal study – Creative Commons BY-SA 4.0 License

You are free to share and adapt this content provided you cite the source